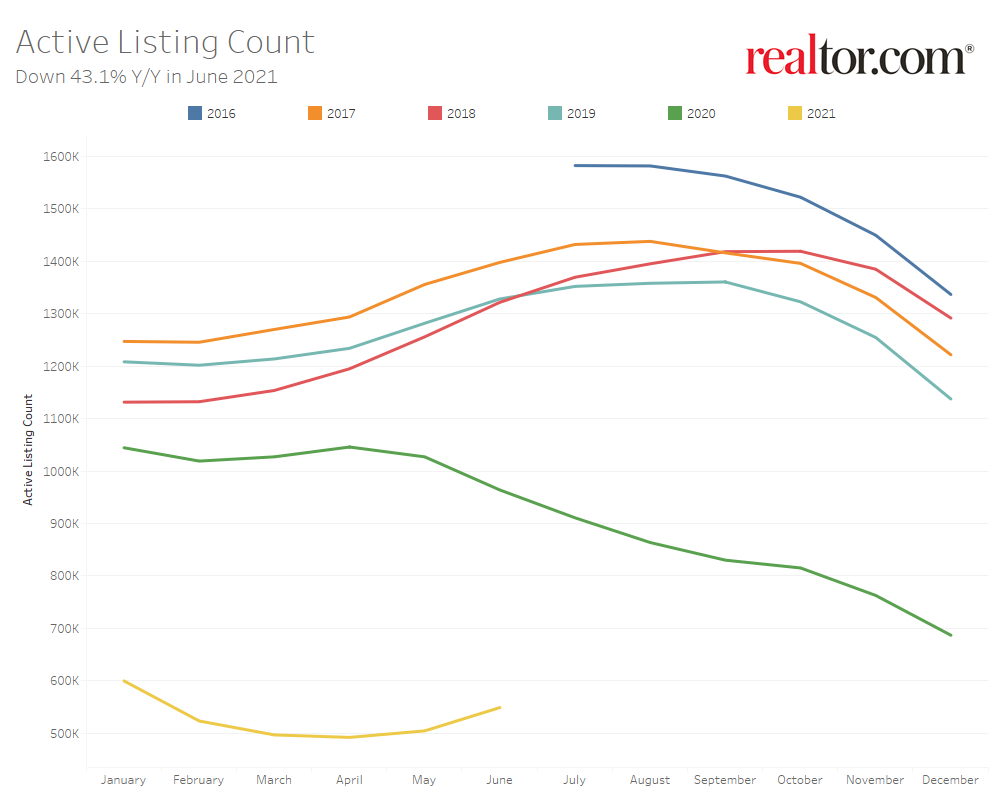

- The national inventory of active listings declined by 43.1% over last year, while the total inventory of unsold homes, including pending listings, declined by 20.3%.

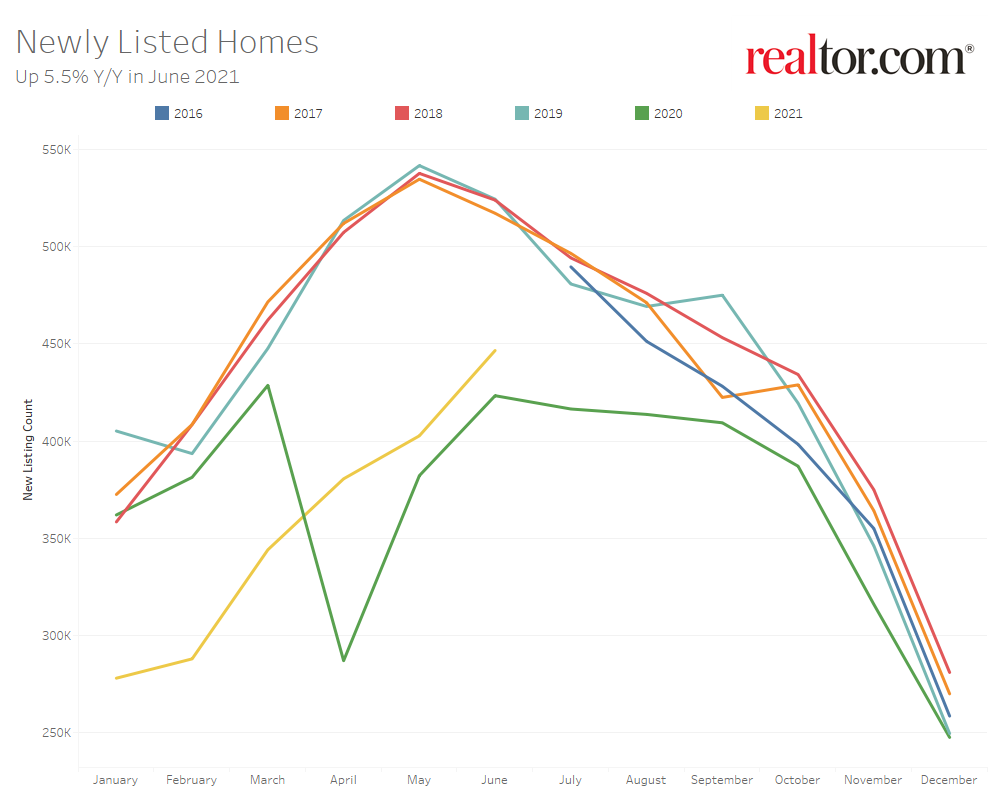

- Newly listed homes on the market are up 5.5% nationally compared to a year ago, and 11.7% higher for large metros over the past year. However, sellers are still listing at rates lower than previous years.

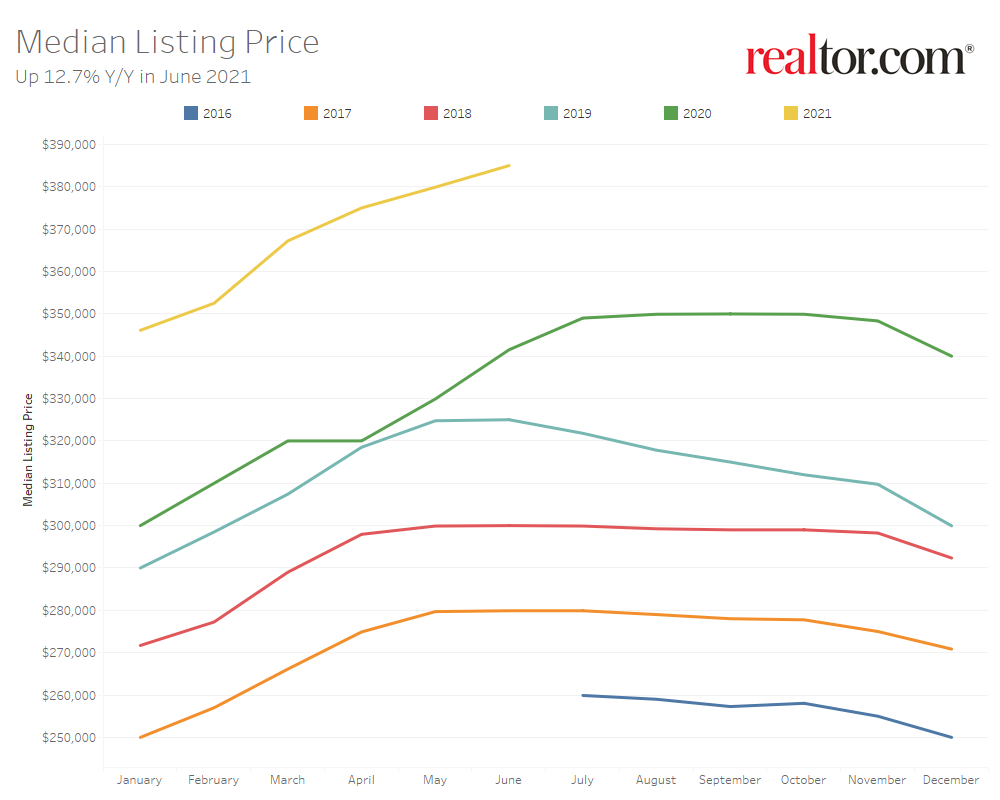

- The June national median listing price for active listings was $385,000, up 12.7% compared to last year. Large metros saw median listing prices grow by 5.3%, on average, compared to last year.

- Nationally, the typical home spent 37 days on the market in June, much less than the 72 days during the same month in 2020.

Realtor.com®’s June housing data release reveals early signs of tempering in the nation’s historically hot housing market. Newly listed homes, while still low, continued to rise in June, diverging from a typical seasonal decline in new listings from May to June. Meanwhile, the inventory of active listings and time on market is decreasing less precipitously, and home listing price growth has decelerated for the second month in a row.

New Listings Increase Over May- A Welcome Sign

Nationally, the inventory of homes actively for sale in June decreased by 43.1% over the past year, a lower rate of decline compared to the 50.9% drop in May. A deceleration in the decline of inventory means the market is heading in an encouraging direction, but active inventory still remains historically low. This decline amounted to 415,000 fewer homes actively for sale on a typical day in June compared to the previous year. The total number of unsold homes nationwide–a metric that includes active listings and listings in various stages of the selling process that are not yet sold– is down 20.3% percent from June 2020.

In June, newly listed homes grew by 5.5% on a year-over-year basis, and by 10.9% on a month-over-month basis. Typically, fewer newly listed homes appear on the market in the month of June compared to May. This year, growth in new listings is continuing later into the summer season, a welcome sign for a tight housing market. However, newly listed homes are still down 14.4% from the typical rate of newly listed homes in 2017 to 2019.

The inventory of homes actively for sale in the 50 largest U.S. metros overall decreased by 40.5% over last year in June, a slowdown in the rate of decline compared to last month’s 49.4% decrease. Regionally, the inventory of homes in southern metros is still showing the largest year-over-year decline. Large southern metros are also seeing the lowest growth in newly listed homes (+4.6%), on average, compared to last year, while newly listed homes in large metros in the Midwest, West, and Northeast, were growing by 19.6%, 18.4%, and 9.9% year-over-year, respectively. In both May and June this year, large Southern metros have not seen many more new listings than the same time last year, which were lower in the South in 2020 much like they were in other regions. By comparison, other regions are either approaching or have reached normal levels seen between 2017 and 2019.

Markets that are seeing the largest year-over-year growth in newly listed homes include Milwaukee (+44.7%), San Jose (+40.7%), and Cleveland (+37.9%). Markets that are still seeing a decline in newly listed homes compared to last year include southern metros such as Nashville (-24.2%), Raleigh (-21.4%), and Miami (-7.8%).

Early Signs of Moderation Appear in Lightning-Fast Market

The typical home spent 37 days on the market this June, more than one month (-35 days) faster than last year, and a new low in recent history. It is also 21 days less than the typical time on market during the June 2017 to 2019 period. Homes are still being quickly snapped up as demand remains elevated, however our weekly data is beginning to show that time on market this year may not consistently decrease beyond seasonal norms like it did last year. In the second-to-last week of June, the median time on market was 33 days lower than the previous year, and for the final week of June, the time on market was 28 days lower than the previous year.

In the 50 largest U.S. metros, the typical home spent 31 days on the market, and homes spent 23 days less on the market, on average, compared to last June. Among these 50 largest metros, the time a typical property spends on the market has decreased most in large metros in the South (-28 days), followed by the Northeast (-22 days), Midwest (-20 days), and West (-17 days).

Among larger metropolitan areas, homes saw the greatest yearly decline in time spent on the market in Miami (-52 days), Raleigh (-48 days), and Pittsburgh (-48 days). No metros saw days on market increase compared to last year in June.

Listing Price Growth Continues to Moderate

The median national home price for active listings reached $385,000 in June and grew by 12.7% over last year, lower than last month’s growth rate of 15.2%. This marks the second month in a row when the annual growth rate has decreased. The slowing rate of growth of listing prices is a welcome sign that the market is moving toward some semblance of balance and that prices may not continue to rise late into the homebuying season as they did last year.

Active listing prices in the nation’s largest metros grew by an average of 5.3% compared to last year, lower than last month’s rate of 7.4%. Price growth in the nation’s largest metros is cooling slightly faster than in other areas across the country. Among the largest 50 metros, listing prices are increasing most in large western markets, where they are now growing at an average rate of 10.8% over last year, compared to a growth rate of 7.2% for southern metros, 4.1% for northeastern metros, and a small -2.9% decline for midwestern metros (largely due to a change in the mix of inventory due to increased newly listed homes).

Austin (+34.3%), Riverside (+19.6%), and Tampa (+19.6%) posted the highest year-over-year median list price growth in June.

Regional Statistics (50 Largest Metro Combined Average)

| Region | Active Listing Count YoY | New Listing Count YoY | Median Listing Price YoY | Median Days on Market Y-Y |

| Midwest | -32.1% | 19.6% | -2.9% | -20 days |

| Northeast | -30.6% | 9.9% | 4.1% | -22 days |

| South | -51.1% | 4.6% | 7.2% | -28 days |

| West | -36.8% | 18.4% | 10.8% | -17 days |

June 2021 Housing Overview by Top 50 Largest Metros

| Metro | Median Listing Price | Median Listing Price YoY | Active Listing Count YoY | New Listing Count YoY | Median Days on Market | Median Days on Market YoY |

| Atlanta-Sandy Springs-Roswell, Ga. | $395,000 | 14.0% | -52.7% | 3.3% | 33 | -20 |

| Austin-Round Rock, Texas | $524,000 | 34.3% | -59.7% | 18.8% | 16 | -33 |

| Baltimore-Columbia-Towson, Md. | $342,000 | -2.1%* | -36.3% | 26.1% | 32 | -18 |

| Birmingham-Hoover, Ala. | $273,000 | -0.9%* | -47.4% | 7.7% | 37 | -25 |

| Boston-Cambridge-Newton, Mass.-N.H. | $699,000 | 6.4% | -25.0% | 13.0% | 22 | -13 |

| Buffalo-Cheektowaga-Niagara Falls, N.Y. | $247,000 | 2.9% | -27.5% | 6.5% | 29 | -21 |

| Charlotte-Concord-Gastonia, N.C.-S.C. | $389,000 | 7.4% | -49.5% | 7.3% | 27 | -29 |

| Chicago-Naperville-Elgin, Ill.-Ind.-Wis. | $355,000 | 4.4% | -31.9% | 3.2% | 33 | -13 |

| Cincinnati, Ohio-Ky.-Ind. | $350,000 | 3.9% | -35.1% | 8.5% | 32 | -19 |

| Cleveland-Elyria, Ohio | $219,000 | -3.4%* | -23.4% | 37.9% | 35 | -27 |

| Columbus, Ohio | $300,000 | -9.8% | -27.2% | 26.2% | 15 | -28 |

| Dallas-Fort Worth-Arlington, Texas | $387,000 | 8.7% | -59.0% | -5.0% | 29 | -19 |

| Denver-Aurora-Lakewood, Colo. | $600,000 | 9.8% | -54.0% | 6.2% | 12 | -24 |

| Detroit-Warren-Dearborn, Mich. | $279,000 | 1.7% | -36.6% | 8.8% | 21 | -18 |

| Hartford-West Hartford-East Hartford, Conn. | $339,000 | 14.9% | -62.9% | -4.6% | 28 | -19 |

| Houston-The Woodlands-Sugar Land, Texas | $366,000 | 12.6% | -43.8% | 7.8% | 36 | -22 |

| Indianapolis-Carmel-Anderson, Ind. | $277,000 | -7.6%* | -43.3% | 17.0% | 34 | -18 |

| Jacksonville, Fla. | $350,000 | 10.2% | -62.6% | -5.5% | 37 | -34 |

| Kansas City, Mo.-Kan. | $332,000 | -7.5%* | -36.6% | 15.2% | 38 | -19 |

| Las Vegas-Henderson-Paradise, Nev. | $400,000 | 18.9% | -48.5% | 8.7% | 25 | -27 |

| Los Angeles-Long Beach-Anaheim, Calif. | $1,025,000 | 5.6% | -26.8% | 10.7% | 44 | -17 |

| Louisville/Jefferson County, Ky.-Ind. | $277,000 | -4.3%* | -36.5% | 19.8% | 24 | -23 |

| Memphis, Tenn.-Miss.-Ark. | $240,000 | -7.2%* | -41.0% | 15.0% | 36 | -21 |

| Miami-Fort Lauderdale-West Palm Beach, Fla. | $447,000 | 11.9% | -51.6% | -7.8% | 62 | -52 |

| Milwaukee-Waukesha-West Allis, Wis. | $300,000 | -18.9%* | -27.6% | 44.7% | 28 | -21 |

| Minneapolis-St. Paul-Bloomington, Minn.-Wis. | $365,000 | -1.3% | -35.2% | 12.7% | 31 | -9 |

| Nashville-Davidson–Murfreesboro–Franklin, Tenn. | $430,000 | 10.2% | -65.3% | -24.2% | 15 | -20 |

| New Orleans-Metairie, La. | $346,000 | 15.4% | -37.4% | 10.5% | 44 | -36 |

| New York-Newark-Jersey City, N.Y.-N.J.-Pa. | $618,000 | 7.0% | -9.4% | -0.9% | 55 | -23 |

| Oklahoma City, Okla. | $285,000 | -2.7%* | -52.8% | -4.4% | 37 | -12 |

| Orlando-Kissimmee-Sanford, Fla. | $356,000 | 11.3% | -57.1% | 1.5% | 36 | -37 |

| Philadelphia-Camden-Wilmington, Pa.-N.J.-Del.-Md. | $335,000 | 2.3% | -21.0% | 24.5% | 37 | -22 |

| Phoenix-Mesa-Scottsdale, Ariz. | $465,000 | 15.8% | -45.8% | 27.8% | 29 | -29 |

| Pittsburgh, Pa. | $262,000 | 6.1% | -37.4% | 1.1% | 40 | -48 |

| Portland-Vancouver-Hillsboro, Ore.-Wash. | $557,000 | 11.4% | -37.9% | 22.6% | 30 | -19 |

| Providence-Warwick, R.I.-Mass. | $425,000 | -1.7%* | -42.5% | 19.5% | 24 | -29 |

| Raleigh, N.C. | $411,000 | 7.0% | -71.7% | -21.4% | 15 | -48 |

| Richmond, Va. | $352,000 | -0.5% | -40.4% | 25.6% | 37 | -20 |

| Riverside-San Bernardino-Ontario, Calif. | $526,000 | 19.6% | -46.5% | 16.0% | 32 | -29 |

| Rochester, N.Y. | $243,000 | -1.9%* | -30.9% | 8.1% | 12 | -17 |

| Sacramento–Roseville–Arden-Arcade, Calif. | $592,000 | 14.5% | -43.1% | 13.1% | 26 | -14 |

| San Antonio-New Braunfels, Texas | $325,000 | 3.8% | -57.9% | 5.0% | 34 | -31 |

| San Diego-Carlsbad, Calif. | $830,000 | 7.5% | -13.3% | 18.4% | 36 | -3 |

| San Francisco-Oakland-Hayward, Calif. | $1,058,000 | 0.8% | -25.3% | 15.0% | 29 | -3 |

| San Jose-Sunnyvale-Santa Clara, Calif. | $1,299,000 | 5.4% | -22.0% | 40.7% | 24 | -12 |

| Seattle-Tacoma-Bellevue, Wash. | $687,000 | 9.8% | -41.2% | 22.7% | 26 | -9 |

| St. Louis, Mo.-Ill. | $258,000 | 3.2% | -34.9% | 16.3% | 43 | -27 |

| Tampa-St. Petersburg-Clearwater, Fla. | $350,000 | 19.6% | -59.1% | 4.0% | 32 | -39 |

| Virginia Beach-Norfolk-Newport News, Va.-N.C. | $315,000 | -4.5%* | -40.9% | 6.9% | 23 | -28 |

| Washington-Arlington-Alexandria, DC-Va.-Md.-W. Va. | $525,000 | -0.9%* | -9.0% | 36.3% | 29 | -8 |

*Median listing price declines in these markets are largely reflective of a change in the mix of inventory due to more newly listed homes being in lower price tiers.

See original article published on Realtor.com here.