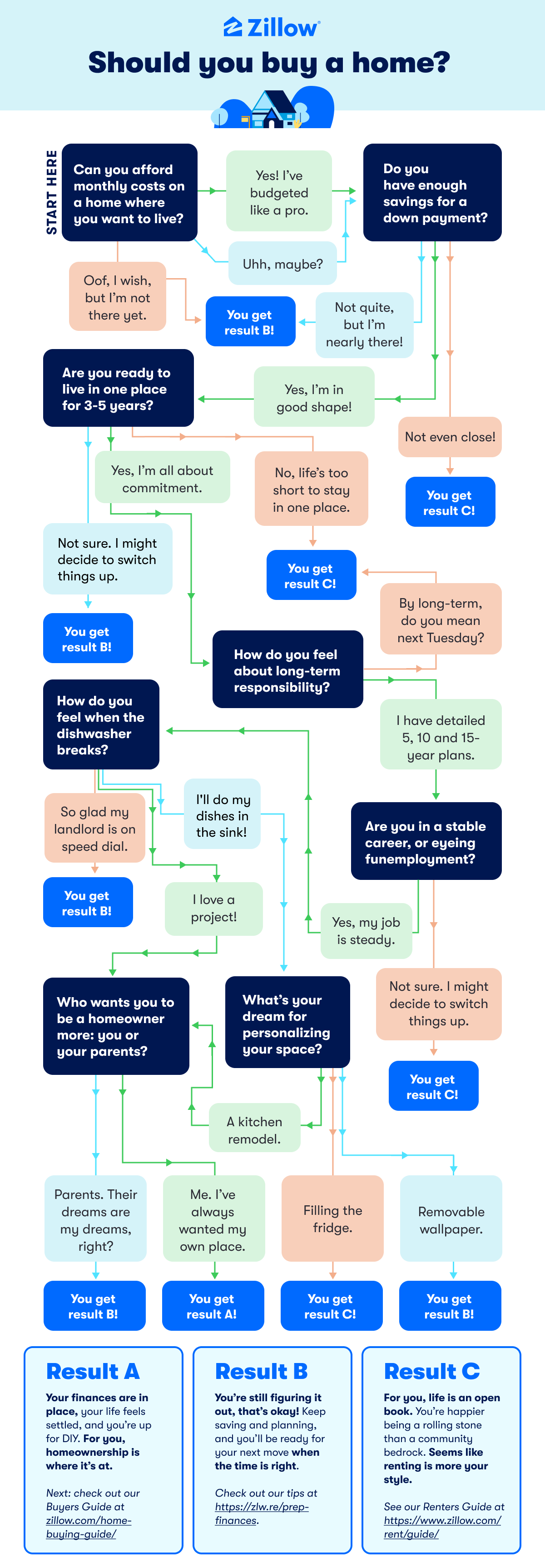

Use this decision tree to answer financial and lifestyle questions that can help you determine whether buying a house is right for you.

Determining when to buy a house isn’t only about your financial readiness, though it is definitely one aspect — a house is probably one of the most expensive purchases you’ll make. Beyond the numbers, you should consider your lifestyle when deciding to buy a house. Homeownership can be a major undertaking that impacts multiple aspects of your day-to-day life.

If you’re still figuring out if you should buy a house, here are both financial and lifestyle signs you may be ready to make such a huge commitment.

Signs you may be financially ready

You have a stable job or source of income

Whether it’s a 9-to-5 job, self-employment income or income from your small business, having regular, steady income is one of the first signs you can commit to a mortgage.

Yes, you’ll need it to pay the bills, but your source of income is one of the main factors mortgage lenders look at when assessing your eligibility for a loan. If you don’t have proof of steady income or have a shaky employment history, you may find it difficult to qualify.

Click the image to enlarge it in a new tab.

You have a down payment

Having enough for a down payment on a home can take a long time to save up, as it can be a huge chunk of money. Depending on the lender and type of home loan, you may be required to put down at least 3% (FHA loans, however, typically require at least 3.5%). For instance, a home that costs $350,000 with a 3% down payment requirement will require you to put down at least $10,500.

Don’t forget to factor in closing costs, which can be anywhere from 2 to 5% of the purchase price.

You have good credit

Lenders look at your credit score as an indicator of whether you’re likely to pay back your debt. The higher your credit score, the more likely you will qualify for a mortgage with the most favorable rates and terms. Even a fraction of a percent higher on an interest rate can mean paying thousands more throughout the life of your loan.

You can afford the costs

Knowing when to buy a house isn’t only about whether you can afford the mortgage, though that’s a major part. It’s also about factoring in other costs such as property taxes, insurance, maintenance and repairs. Between all that, you’ll need to make sure you can also afford your lifestyle, such as bills, entertainment and other financial goals, and be able to make adjustments as needed.

You can use a mortgage or housing affordability calculator to determine how much you may be able to afford. If you can do so comfortably, it’s a sign you’re ready for homeownership.

You have a good debt-to-income ratio

In addition to your income, mortgage lenders also look at your total debt. They look at your debt-to-income ratio, or DTI, to determine whether you can afford to take on a new loan in addition to your existing debt. The higher your DTI, the more likely you’ll be stretched too thin financially.

For this reason, lenders typically want borrowers to have a DTI of around 36% or less. To calculate your DTI, total all your monthly debt payments and divide it by your gross monthly income. If your DTI hovers around 36% (the lower, the better), you can probably afford a mortgage.

Signs you are personally ready

You have no short-term plans to move

Buying a house is typically a commitment to a specific location or neighborhood — if you love the area and can afford it, then fine. However, you also need to account for the fact you’ll most likely need to stay in your home for at least several years to see any return on investment when you do sell.

Plus, buying and selling a house takes time and money beyond the cost of the house itself. Unlike renting, where you end your contract and move your belongings, selling a house requires an additional financial commitment — think listing agent and other closing fees. It could also take months before you find a buyer and move. So if you’re ready to stay put, the extra work involved to buy a house could be worth it.

You have the bandwidth to engage in handyman skills

Owning a home means you won’t have a landlord who you can call if you need repairs done around the house. In other words, you need to ensure you have time to maintain your home and to learn the skills to do so. It’s not only plumbing work or fixing cracked windows; maintenance also includes routine tasks like mowing and fertilizing the lawn.

If you don’t have the skills or time to learn them, it means taking the time to hire a reputable contractor and oversee their work.

Take a careful look at your schedule to see whether it isn’t too demanding for you to take a few hours here and there to maintain your home. Be realistic; even if it’s a relatively new or move-in-ready home, you’ll need to give up some free time to keep your home in tip-top shape.

Be realistic; even if it’s a relatively new or move-in-ready home, you’ll need to give up some free time to keep your home in tip-top shape.

You aren’t feeling pressured

For some, owning a home isn’t all that attractive, but they become a homeowner because of peer pressure. Perhaps your parents are wondering whether you’ll stop throwing money away on rent (in their words), or you keep seeing beautiful photos of homes your friends and co-workers have bought and renovated on social media.

If the decision to own a home is yours and yours alone, that’s great. Otherwise, you’re probably better off waiting if you feel you should purchase a home because that’s what people are telling you to do.

You’re ready to commit

Homeownership takes up a large portion of your time and budget, so you want to be absolutely sure you’re ready to commit. For example, if you’ve got other major life decisions you might want to make, such as long-term travel, taking a work sabbatical or going back to graduate school, then it might be better to put off buying a home. However, if you really want to invest in a place that will grow with you, then by all means, consider buying a home.

So, should you buy a home? Answer the questions in the decision tree to help you decide.

Then, visit our Buyers Guide, Renters Guide, or read our tips for planning your finances to get ready for your next move — wherever that may be.