Even seemingly small changes in mortgage rates, like 1% or 0.5%, can make a big difference in what you pay over the life of your loan.

When you’re sizing up a home to buy, it’s tempting to focus only on the price to decide whether it fits your budget. But current mortgage rates are an equally large part of the affordability equation — and they probably changed since you last did the math. Mortgage interest rates change frequently, and even seemingly small changes in rates can affect not only what you’ll pay for housing each month and over the long run, but how much you can afford to spend on a home.

Given the extraordinary volatility of the mortgage market over the past two years, it helps to know how interest rates impact what you can afford — and how you can keep on top of rates so you’re getting the best possible deal.

How does the mortgage rate affect your monthly payment?

When you pay your mortgage every month, you’re paying down the amount you borrowed — known as the principal, and the interest on that money. The payments follow a fixed schedule, with the earlier payments consisting mostly of interest. Over time, a greater share of the payment goes toward the principal until your home is paid off or you refinance your loan or sell your home.

Olsen says even small changes in mortgage interest rates can save you — or cost you — money every month, and affect your purchasing power. “Those mortgage rates really do matter,’’ Olsen says. “Depending on your price point, even a half percentage point can increase or decrease the number of opportunities you can afford to move forward on.”

How much of a difference does 1% make on a mortgage rate?

To give you an idea of how changes in mortgage rates affect your monthly payment and your purchasing power, we looked at changes in rates through the lens of a buyer searching for a typical home. We looked at a typical home nationally and in specific metros. In each case, we assume that the buyer is putting 20% down toward the purchase and is financing the purchase with the most common loan type: a fixed-rate, 30-year mortgage. These calculations do not include taxes and insurance.

A typical U.S. home, valued at $346,900: $182 a month

At a 7% mortgage rate, your monthly payment would be $1,846. At 6%, it’s$1,664, or $182 less each month. Over 30 years, the difference would save you $65,691 in interest.

Buying power boost:If you budgeted about $1,846 a month for a mortgage payment, and the interest rate dropped 1 percentage point — from 7% to 6% — you could spend about $30,480 more on a home without increasing your monthly payment.

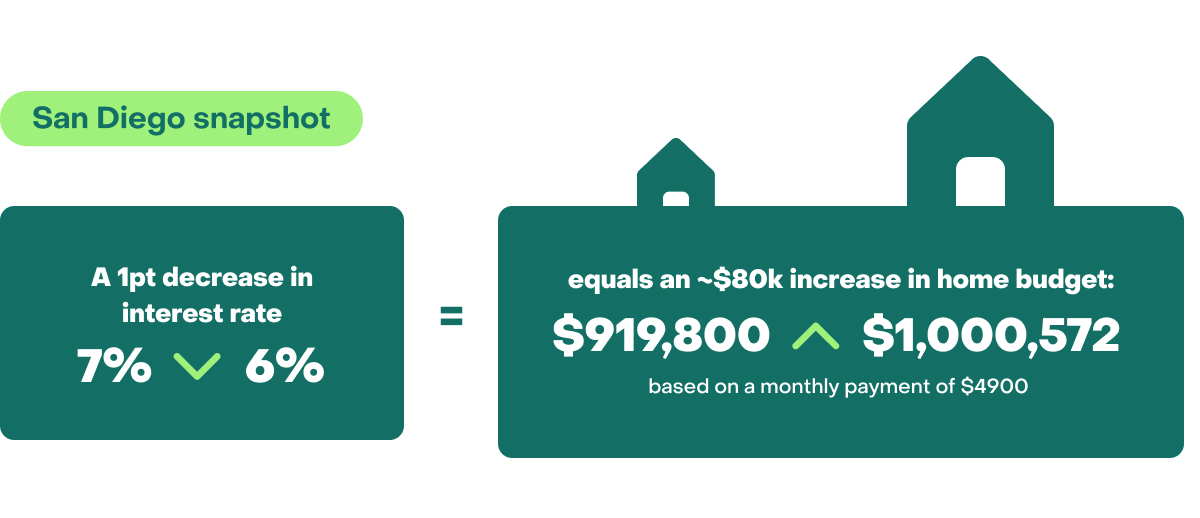

A typical home in San Diego, valued at $919,800: $484 a month

At a 7% mortgage rate, your monthly payment would be $4,896. At 6%, it’s $4,412, or $484 less each month. Over 30 years, the difference would save you $174,178 in interest.

Buying power boost: If you budgeted $4,896 a month for a mortgage payment, and the interest rate dropped 1 percentage point — from 7% to 6% — you could spend about $80,772 more on a home without increasing your monthly payment.

A typical home in Atlanta, valued at $375,100: $197 a month

At a 7% mortgage rate, your monthly payment would be $1,996. At 6%, it’s $1,799, or $197 less each month. Over 30 years, the difference would save you $71,030 in interest.

Buying power boost: If you budgeted $1,996 a month for a mortgage payment, and the interest rate dropped 1 percentage point — from 7% to 6% — you could spend $32,920 more on a home without increasing your monthly payment.

A typical home in Dallas, valued at $371,300: $195 a month

At a 7% mortgage rate, your monthly payment would be $1,976. At 6%, it’s $1,781, or $195 less each month. Over 30 years, the difference would save you $70,321 in interest.

Buying power boost: If you budgeted $1,976 a month for a mortgage payment, and the interest rate dropped 1 percentage point — from 7% to 6% — you could spend $32,540 more on a home without increasing your monthly payment.

A typical home in St. Louis, valued at $241,500: $127 a month

At a 7% mortgage rate, your monthly payment would be $1,285. At 6%, it’s $1,158, or $127 less each month. Over 30 years, the difference would save you $45,735 in interest.

Buying power boost: If you budgeted $1,285 a month for a mortgage payment, and the interest rate dropped 1 percentage point — from 7% to 6% — you could spend $21,127 more on a home without increasing your monthly payment.

A typical home in Pittsburgh, valued at $202,000: $106 a month

At a 7% mortgage rate, your monthly payment would be $1,072. At 6%, it’s $966, or $106 less each month. Over 30 years, the difference would save you $38,138 in interest

Buying power boost: If you budgeted $1,075 a month for a mortgage payment, and the interest rate dropped 1 percentage point — from 7% to 6% — you could spend $13,402 more on a home without increasing your monthly payment.

How much of a difference does 0.5% make on a mortgage rate?

To see how even a half a percentage point can change what you pay monthly and over time, let’s look at a few other metros.

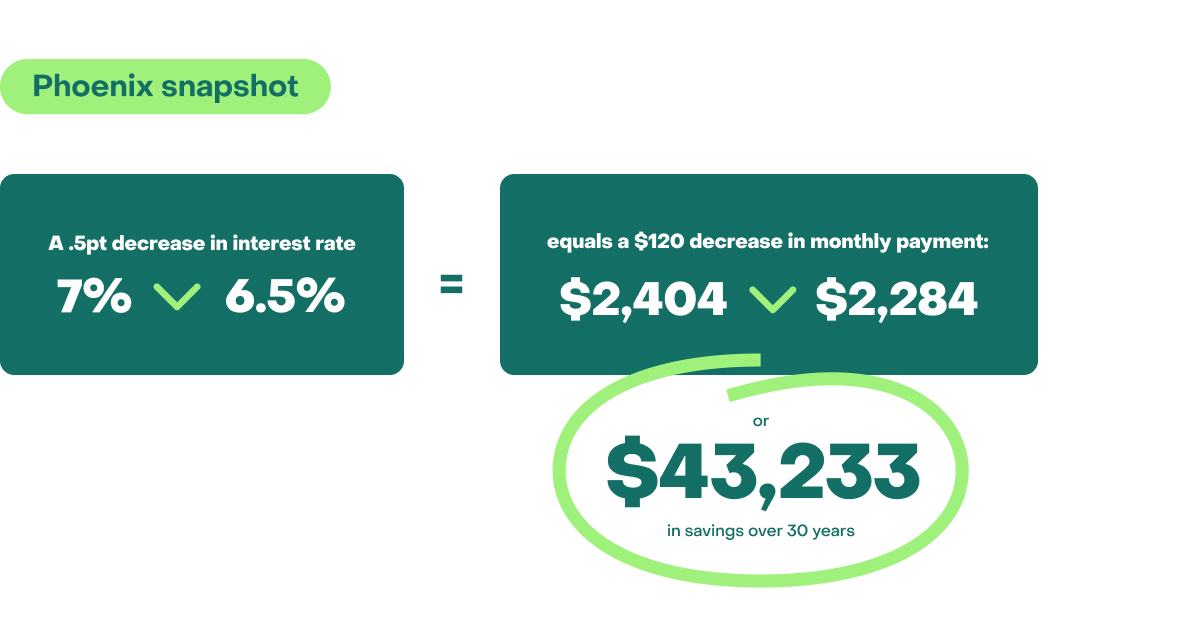

A typical home in Phoenix, valued at $451,600: $120 a month

At a 7% mortgage rate, your monthly payment would be $2,404. At 6.5%, it’s $2,284, or $120 less each month. Over 30 years, the difference would save you $43,233 in interest.

Buying power boost: If you budgeted $2,404 a month for a mortgage payment, and the interest rate dropped half a percentage point — from 7% to 6.5% — you could spend $19,059 more on a home without increasing your monthly payment.

A typical home in Portland, Oregon, valued at $524,870: $140 a month

At a 7% mortgage rate, your monthly payment would be $2,794. At 6.5%, it’s $2,654, or $140 less each month. Over 30 years, the difference would save you $50,238 in interest.

Buying power boost: If you budgeted $2,794 a month for a mortgage payment, and the interest rate dropped half a percentage point — from 7% to 6.5% — you could spend $22,145 more on a home without increasing your monthly payment.

A typical home in Cincinnati, valued at $270,800: $72 a month

At a 7% mortgage rate, your monthly payment would be $1,441. At 6.5%, it’s $1,369, or $72 less each month. Over 30 years, the difference would save you $25,919 in interest.

Buying power boost: If you budgeted $1,441 a month for a mortgage payment, and the interest rate dropped half a percentage point — from 7% to 6.5% — you could spend $11,342 more on a home without increasing your monthly payment.

A typical home in Las Vegas, valued at $411,600: $110 a month

At a 7% mortgage rate, your monthly payment would be $2,191. At6.5%, it’s $2,081, or $110 less each month. Over 30 years, the difference would save you $39,392 in interest.

Buying power boost: If you budgeted $2,191 a month for a mortgage payment, and the interest rate dropped half a percentage point — from 7% to 6.5% — you could spend $17,360 more on a home without increasing your monthly payment.

Tips for dealing with volatile mortgage rates

Mortgage rates are notoriously hard to predict, making it difficult to time a purchase to capture a better interest rate. But there are some things you can do.

Plan flexibility in your budget early on

Are you shopping at the top of your budget or are you giving yourself room in case the rates change while you’re shopping? Having flexibility also allows you more options if you get into a competitive bidding situation.

Pro tip: Use the Affordability Calculator to see how your shopping budget changes under different scenarios.

Talk to lenders

Find a lender you trust who can walk you through financial scenarios, including options to buy down the interest rate. Doing so can help you act quickly if you find a home to buy. Learn more about when you should buy down your interest rate.

Prep your finances

Focus on getting your credit score in the best shape possible since lenders usually reserve their best rates for borrowers with higher credit scores.

Consider locking in your mortgage rate with your lender

Changing rates can make it hard to tell when to lock in your mortgage rate. For most home shoppers, it’s generally best to lock your rate after you sign an agreement to buy a home.

Shop around when looking for rates since rate lock fees can vary among lenders. And watch the timing since you could lose your rate if your loan doesn’t process in the time period called for in the sales contract.

Consider whether to refinance

Some shoppers opt to buy at one rate with plans to refinance when rates drop. This option has costs attached to it, with average refinance closing costs ranging between 2%-6% of the loan amount. And, again, rates are hard to predict. Try our Refinance Calculator to see what a refinance might look like for you.

Mortgage interest rate FAQs

Will mortgage rates drop?

The days when mortgage rates dipped below 3% are long gone, and no one expects their return, says Zillow Chief Economist Skylar Olsen. Instead, we’re likely to see fluctuations around higher rates as the Federal Reserve Board tries to control inflation by raising and lowering a key interest rate that influences the rates mortgage lenders offer.

“These days, rates bounce up and down with the jobs report, the inflation numbers and fed meetings,’’ Olsen says. “Mortgage rates should ease, but probably not until the end of the year if not next. Until then, buyers and sellers should be planning for the same kind of volatility in 2024.”

Should you wait for mortgage rates to drop to buy a house?

No one knows what’s going to happen to interest rates, so there are no guarantees they’ll come down, how much they’ll drop or if increasing home prices will wipe out any savings you might have gained.

Also, there are still more shoppers than homes for sale, so you might not have the luxury of waiting for a rate drop if you find a home you want, Olsen says.

“Buyers will want to try to time their purchase with a low mortgage rate window so they should start to build relationships with a couple of lenders early on,’’ she says. “But please don’t discount your opportunity to refinance later on if you find the right home now. Supply is ultimately very low.”